Current Market Environment

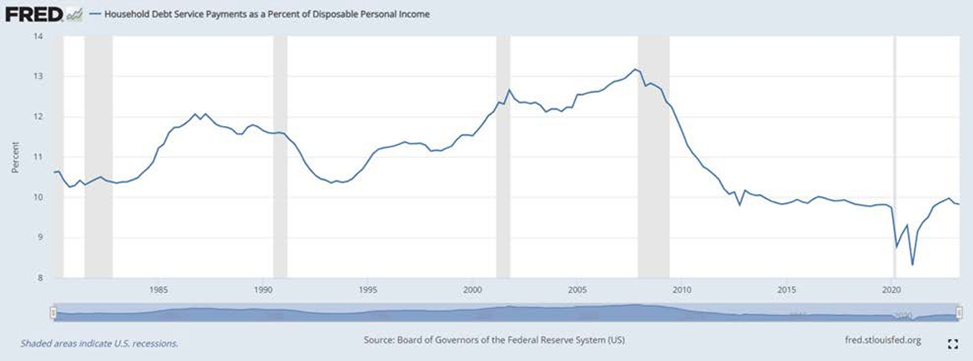

In the third quarter, the market seemed to grapple with a "higher for longer" interest rate environment. The benchmark 10-year Treasury rose significantly during the quarter (from 3.81% to 4.57%), causing unease for investors, and contributing to the market’s decline during the period. Given the sharp rise in interest rates, sectors which traditionally carry higher dividend yields and/or higher levels of debt were hit hardest. This included utilities, real estate, and consumer staples stocks. Inflation, while continuing to print lower year-over-year increases, remained persistently above the Federal Reserve’s 2% target. Indeed, recent core inflation readings remain closer to 4%. Meanwhile, the U.S. consumer remains resilient, and spending continues at fairly robust levels, resulting in recession forecasts being pushed ever farther into the distance. That said, there are underlying signs of consumers pulling back – especially the low-end consumer. Retailers have noted customers trading down to private label brands, or smaller pack sizes for example. Additionally, banks and other companies with finance arms have noted credit trends are beginning to “normalize” from ultra-low levels aided by pandemic-related stimulus. Indicative of this, Macy's stock was hit hard in August when they announced a concerning rise in credit card delinquencies. Clearly, impacts are starting to be felt from the drying up of pandemic-related excess savings. However, as can be seen in the chart below, consumer balance sheets remain relatively healthy, and overall debt service payments, for the time being, remain low relative to history.

Over time, the historic rise in interest rates could further strain the consumer. Currently, most homeowners hold mortgages with a rate below 4% (to be specific, 72% of borrowers locked in below 4% according to Goldman Sachs). This is contributing to the current logjam in the housing market, as the prospect of a mortgage closer to 8% is daunting. Over time though, life changes often necessitate moves, and resultant mortgages will require higher debt service payments. Similar could be said for auto loans, which have risen from 5.5% last summer to almost 8.5% in just over a year (for a 48-month term).

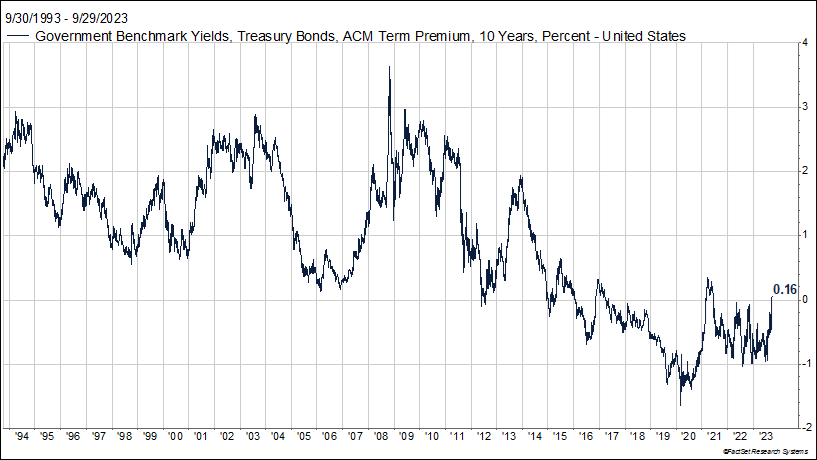

In addition to the stronger than expected economy and persistently high inflation, market followers and pundits have recently become concerned with the concept of "term premium" and the potential for rising term premiums to be a contributing factor to a higher for longer interest rate environment. The term premium, which is the extra yield investors demand to compensate for risks implicit in buying a longer- term bond, has recently turned positive after spending the better part of the past five years in negative territory. However, as can be seen in the chart below, the term premium on the 10-year Treasury has historically been significantly higher for long periods at a time. In fact, according to the Wall Street Journal, the term premium has added an average 1.5% to 10–year yields since 1961.

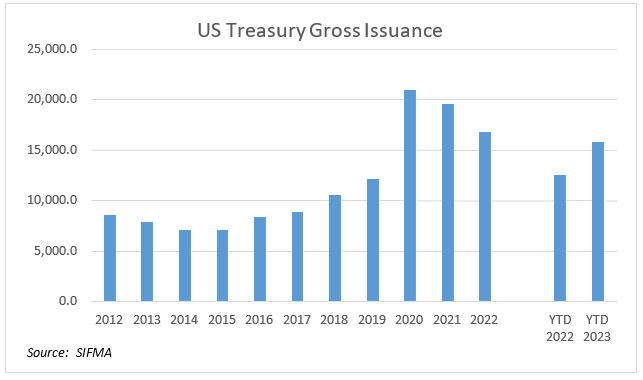

It is, of course, difficult to determine what exactly has caused the term premium on long-term bonds to increase. One reasonable explanation, given the higher interest rate backdrop, is concerns about the rising level of federal debt and deficit funding. The U.S. government has issued $15.7 trillion in bonds through September, up from $12.5 trillion through the same point last year and on track to reach the record levels seen in 2020. Issuances are anticipated to increase a further 23% in 2024 according to Barron’s. Could rising deficits, and ever-increasing levels of U.S. debt finally matter to fixed income investors? Only time will tell; but, if term premiums continue to rise, interest rates could head even higher from here.

GLP-what?

Much as artificial intelligence (AI) dominated headlines and investor mindshare earlier in the year, in the third quarter, the market became fixated on the impacts of GLP-1 drugs. These drugs (GLP is short for glucagon-like peptide) include Novo Nordisk's Ozempic and Wegovy, as well as Eli Lilly's Mounjaro, and also several others in development. Originally developed to treat diabetes, they are increasingly being used to treat obesity as patients prescribed the medications have shown substantial weight loss. Additionally, recent results have indicated these drugs substantially curb cravings not only for food but also things like soft drinks, alcohol and tobacco. Given the high level of obesity in the United States, these drugs could obviously have a significant impact on food consumption. Additionally, it could be extrapolated that demand for orthopedic, heart, and other medical procedures impacted by being overweight could see reduced demand. Given this, as can be seen in the chart below, food-related stocks, restaurants, and medical device stocks have sold off en masse as these drugs and their effects dominated headlines during the summer months (peak Google search trends for the term "Ozempic" were seen in June).

Much like the AI frenzy during the spring, where seemingly everything AI-related was bid up, the market took a similar (but directionally opposite) approach with the food and medical device stocks - shooting first and asking questions later. For bottom-up stock pickers like ourselves, this creates opportunities to sift through the rubble and find oversold names. There are, for example, offsetting potential positives for many of these companies which need to be considered. For example, the knee-jerk reaction is to believe a reduced overweight population will result in less need for knee and hip surgeries. But, this could be offset by having a larger percentage of the population eligible for such surgeries if their BMI (body mass index) comes inline with guidelines. Additionally, a second derivative of losing weight could be increased exercise and other physical activity, potentially resulting in injury. It is very early days, and hard to know the ultimate impact from these drugs. However, on Abbott Laboratories’⁽¹⁾ (ABT - a long position in the LS Opportunity Fund) recent earnings call, CEO Rob Ford stated that despite all of the negativity surrounding their diabetes-related products, including continuous glucose monitors, the data so far has actually shown an increased usage of their Libre sensors from diabetics who are undergoing GLP-1 treatments. This is counter to the doom and gloom implied by recent ABT share performance.

When it comes to the impact on food-related companies, Morgan Stanley estimates that overall calorie consumption could decline in the U.S. by 1-2% by 2035. This seems manageable, especially in the context of things that happen in the ordinary course of a business cycle such as impacts from increased competition, or pricing changes for example. And all calories are not created equal. Companies which heavily skew to sugary snacks or “junk” food will almost certainly be more adversely impacted, as will fast- food restaurants. Additionally, data suggests that consumers of these drugs are experiencing a substantial loss of muscle mass, with over 30% of weight loss being attributed to reduced muscle mass in some studies. That could dissuade some from long-term use of these drugs or from taking them altogether. Interestingly, both ABT and Nestlé⁽²⁾ (NESN-SWX, also a long position in the LS Opportunity Fund) recently indicated they are in the process of developing products specifically targeted to those who have lost muscle mass due to the drugs, hoping to offset potential lost revenue from the GLP-1 effect.

Portfolio Implications

Related to the aforementioned elevated interest rate environment, as discussed in prior letters, Prospector has been in the “higher for longer” camp for quite some time. And, although we are bottom- up investors, the macro environment plays some role in shaping our views on certain stocks or sectors. For example, we remain very selective on banks due to the potential for further strains on the consumer and, at a minimum, a normalization of credit trends. As discussed in last quarter's letter, we also continue to be leery of the low-end consumer, and maintain short positions in companies exposed here. That said, we do not see a recession in the near term, and maintain a fairly balanced portfolio overall. During the third quarter, we continued to opportunistically add to some cyclical holdings which have underperformed due to inventory destocking and, in some cases, we feel are already discounting a slowing economy.

In terms of stocks impacted by GLP-1 drugs, given the near universal selloff of food-related and medical- device companies, there are certain to be opportunities. The LS Opportunity Fund’s portfolio has recently been underweight consumer staples given what we thought were overly demanding valuations as well as the prospect of facing tough comparisons from significant price increases over the past year. On the margin, the GLP-1 related selloff has made the sector more attractive, but we have not made material changes as of yet. Should we deem it appropriate to be more defensively positioned, or if these stocks continue their declines, it is likely we would be more constructive on the sector. In certain cases, the selloff in medical device companies appears overdone. Given this, we have recently increased exposure slightly via a partial short cover within the sector. We continue to look for opportunities to increase exposure here. Finally, we had reduced our modest exposure to restaurants earlier in the year, based on strong performance and our concerns of a consumer pullback. We are likely to look to add to high-quality names which are now trading at more attractive multiples following the recent selloff.

Outlook

Over the last year and a half, the Federal Reserve has aggressively raised interest rates in an effort to lower inflation, causing significant uncertainty within stock and bond markets. Markets seem likely to remain volatile until interest rate increases are behind us, and the resulting impact on the economy is more foreseeable. The U.S. and rest of the world continue to manage the impacts of high inflation, geopolitical events and stresses within the banking system. In our assessment, the probability of Federal Reserve policy error and / or recession has increased, though barring extraneous events, we still lean towards slowdown and not recession per se as noted above.

The biggest risk right now would seem to be from a “shock to the system” during this period of relative weakness while we are troughing the transition from the pandemic economy to a more normalized economy. Certainly, the traumatic events in Israel in recent weeks, and the risk of potential systemic shock that might spread from the Middle East in the months to come, keep us up at night as we are sure they do you as well. As always, with our bias towards quality, we strive to mitigate any downside, while also participating in the upside.

Meanwhile, employment remains strong. Heavy fiscal stimulus from already passed U.S. legislation for defense, infrastructure, semiconductors, and energy investment are only now beginning to be awarded. The spending will not peak until later in the decade. Relatively high energy costs in Europe, and Germany in particular, makes manufacturing here relatively more attractive. Political risk in China makes that country less attractive to do business in. All told, U.S. manufacturing is being called upon to step up. Barring a major crisis, Ronald Reagan’s termed “willing workers” should be able to find jobs…and pay their bills. Furthermore, supply / demand imbalances in the labor market suggest further wage gains to come which will partially mitigate the impact of inflation on the consumer. We expect continued pressure on housing prices as a result of higher interest rates and affordability concerns. However, the shortage of housing after over a decade of underinvestment following the Great Financial Crisis should prevent a disastrous decline in home prices. Lower-income consumers have been most impacted by the current inflationary environment, but consumer balance sheets remain generally healthy for the majority of Americans, and consumer credit quality remains strong at the moment. COVID-related headwinds continue to dissipate.

While what we see argues for a more inflationary and higher interest rate environment than seen in the past ten years, it also does not argue for a recession. Nonetheless, the unexpected can occur. Should a recession happen in the near term, the factors highlighted above suggest it could be less significant than the previous two recessionary periods.

Following years of lower interest rates helping to drive ever-higher growth-stock valuations, we feel value investing is ripe for a period of outperformance. We continue to find opportunities to invest in quality businesses with solid balance sheets and cash flows, whose share prices have detached from our assessment of the fundamentals. The bargains inherent in the LS Opportunity Fund’s portfolio should attract acquirers and other investors over time.

Steadfast, we remain committed to making you money while aiming to protect your wealth.

(1) As of September 30, 2023, ABT position represented 1.0% of the portfolio.

(2) As of September 30, 2023, NESN-SWX position represented 1.0% of the portfolio.

Disclaimer:

The information presented should not be considered a recommendation to purchase or sell any particular security. There can be no assurance that any securities identified herein will remain in the Fund’s portfolio or, if sold, will not be repurchased. The securities identified do not represent the Fund’s entire portfolio and in the aggregate may represent only a small percentage of the Fund’s portfolio holdings. It should not be assumed that any of the holdings identified have been or will be profitable, or that recommendations made in the future will be profitable.

Past performance is not a guarantee of future results.

Important Risk Information

Investment in shares of a long/short equity fund have the potential for significant risk and volatility. A short equity strategy can diminish returns in a rising market as well as having the potential for unlimited losses. These types of funds typically have a high portfolio turnover that could increase transaction costs and cause short-term capital gains to be realized. The stocks in the Fund’s portfolio may decline in value or not increase in value when the stock market in general is increasing or decreasing in value and you could lose money. The Fund may lose money due to fluctuations within the stock market which may be unrelated to individual issuers and could not have been predicted. The price of the securities which the Fund holds may change unpredictably and due to local, regional, international, or global events. In the case of a general market downturn, multiple asset classes, or the entire market, may be negatively affected for an extended and unknown amount of time.

Prospector Partners, LLC assumed investment management duties on 05-28-2015 and was formally approved by shareholders on 09-17-2015.

The Fund is distributed by Ultimus Fund Distributors, LLC. (Member FINRA).

17533523-UFD-10/31/2023