The Rate Outlook

The Federal Reserve opted for a 75-basis-point increase in the update data Fed Funds Rate in June. This was higher than its previous guidance of 50- basis points. This is accredited to the higher than expected inflation figure for May. The central bank risks being stuck behind the 8-ball on inflation as consumer expectations of inflation keep rising.

The Fed sees these expectations as a self-fulfilling prophecy because workers will demand higher wages to keep pace with inflation, furthering the inflationary cycle. After insisting inflationary pressures were transitory for the better part of last year, the Fed wants to regain its inflation-fighting credibility. The rise in consumer inflation expectations is showing it is struggling to do this. What does this mean? It means the Fed will potentially have a higher resolve to bring down inflation, potentially leading to larger rate increases. If this is the case, it will mark a stark contrast with the monetary policy implemented after the ’08 crash through 2021.

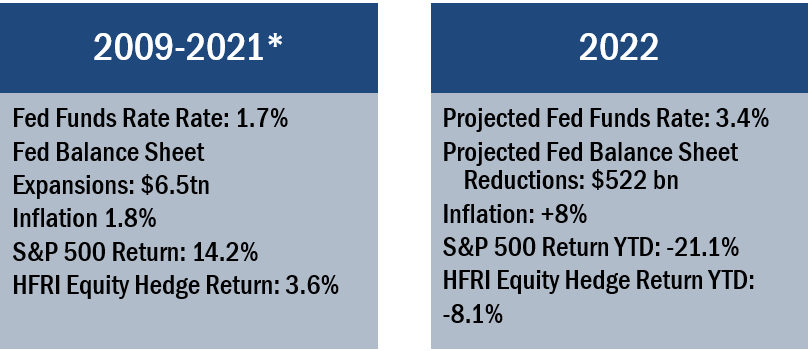

Figure 1: Shifting Monetary Environment

Figure 1 details Fed policy stances from ’09-’21 and expected policy rates at the end of ’22. Some key takeaways from this year’s projection are higher rates leading to more expensive borrowing, less credit in the market leading to less lending, and high inflation. The market reacted accordingly to these realizations; it sees the policies as a potential headwind to businesses, helping contribute to the S&P 500’s steep decline. On the other hand, during ’09-’21, when the Fed pumped money into the economy, the S&P 500 saw annualized returns of 14%.

Long Short’s Performance

Another important point from Figure 1 is HFR’s long short index, HFRI Equity Hedge, during these different environments. During the ’09-’21 period, long short underperformed the S&P 500 by 10.6%. The monetary environment was likely a large reason for this. A rising tide lifted all boats; the broader market was mostly spared from steep declines because of the aid the Fed was providing to the economy. As a result, long short funds’ shorts underperformed and their cash accounts were not yielding interest, dragging down fund-wide performance. Now, however, the market is potentially pointing to a higher rate environment. Long short has benefitted from this sentiment as it is outperforming the S&P 500 by 13% this year.

There are several reasons long short is well positioned to gain in a rising rate environment. The first being, not all stocks will rise. Some companies will struggle to generate earnings if their balance sheets are not prepared for higher rates. A long short fund has the opportunity to generate return on companies who will struggle due to its ability to short stocks. The potential to either significantly reduce downside or gain when the broader market declines is invaluable as rate hiking periods historically coincide with a decline in equities. Additionally, as rates rise, the cash proceeds generated from short sales will earn higher and higher yields on cash through interest payments, further contributing to returns and reducing beta. Thus, in this environment, investors have potentially multiple ways to win with long short that they may otherwise not have with a long-only strategy.

HFRI Equity Hedge (Total) Index Description: Equity Hedge: Investment Managers who maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios. EH managers would typically maintain at least 50% exposure to, and may in some cases be entirely invested in, equities, both long and short. The HFR Indices are compiled by Hedge Fund Research, Inc. and are not investable products. The HFR Indices are being used under license from HFR, Inc., which does not approve of or endorse any of the products or he contents discussed in this material. Source: HFR, Inc. www.HFR.com.

15280562-UFD-07/07/2022